The Cheapest Way to Get GLP-1 — With or Without Insurance

The cheapest way to get GLP-1 is almost never the number most people see first is somewhere north of $1,000 per month — often well above that, depending on the pharmacy and the dose. Those numbers are real. They are also, for most patients, almost completely irrelevant.

In 2024, researchers followed 4,066 commercially insured adults with obesity who had been prescribed a GLP-1 medication. By the one-year mark, only 32% were still on therapy. The two leading reasons: cost and side effects. Not lack of efficacy. Not preference. Cost.

A medication that is too expensive to sustain is a medication that does not work.

The sticker price is not the real price. What you actually pay for a GLP-1 medication depends almost entirely on which door you walk through — your insurance status, the savings programs you know about, the pharmacy you choose, and the platform you use to get the prescription. This article maps every door, from the most expensive to the least.

In This article

What Branded GLP-1 Medications Actually Cost

Before exploring your options, the baseline matters.

Wegovy (semaglutide, weekly injection) and Zepbound (tirzepatide, weekly injection) both carry retail list prices that run well over $1,000 per month at a standard pharmacy without any savings program. The exact figure varies by dose, pharmacy, and whether you are filling the injection pen or the newer pill formulation.

For a full head-to-head comparison of semaglutide vs tirzepatide — including their cost structure and clinical differences — see Semaglutide vs Tirzepatide: What the Data Actually Shows.

The gap between these sticker prices and what patients actually pay can be as wide as $1,300. What closes that gap is navigational knowledge — which is exactly what the rest of this article provides.

If You Have Commercial Insurance

For patients with employer-sponsored or private insurance, coverage is the first variable to investigate — but “covered” does not always mean affordable.

Prior authorization. Most insurance plans require prior authorization for GLP-1 medications. Your prescriber submits documentation demonstrating medical necessity — typically a BMI of 30 or greater, or 27 with a qualifying comorbidity such as type 2 diabetes, hypertension, or metabolic syndrome. This process can take several days to several weeks.

Formulary tier and step therapy. Even when covered, GLP-1s for weight management typically sit on specialty tiers, which carry the highest cost-sharing. Some plans also require step therapy — meaning you must first try and fail at least one other medication before GLP-1 coverage is approved.

The coverage gap. As of 2024, fewer than half of employer-sponsored health plans covered GLP-1s specifically for obesity treatment. Coverage is more consistent when the indication is type 2 diabetes. If your plan does not cover weight management GLP-1s, the appeal process is worth pursuing — but you will need documentation, persistence, and your prescriber’s support.

If your insurance denies coverage, request a formal denial in writing. Your prescriber can assist with an appeal. If the appeal fails, the options below become your primary path.

Manufacturer Savings Programs — The First Door Most People Miss

Both major manufacturers — Novo Nordisk and Eli Lilly — offer patient savings programs for commercially insured patients. These programs are not prominently advertised — which is exactly why they are the first thing to check.

Wegovy Savings Offer (Novo Nordisk): Commercially insured patients may pay as little as $25 per month, with manufacturer savings capped at $100 per month. For patients without insurance, Novo Nordisk also offers direct self-pay pricing through NovoCare Pharmacy — starting at $149 per month for the pill formulation and $199 per month for the pen (introductory pricing; rates are scheduled to change after mid-2026). Enrollment at novocare.com or by texting SAVE to 83757.

Zepbound Savings Card (Eli Lilly): For commercially insured patients whose plan covers Zepbound, the out-of-pocket cost can be as low as $25 per month, with maximum savings of $100 per month and an annual cap of $1,300. For patients with commercial insurance that does not cover Zepbound, the savings card brings the KwikPen price to a starting point of $299 per month. Card expires December 31, 2026.

Who is eligible — and one important clarification: These programs exclude patients on Medicare, Medicaid, VA, TRICARE, or any federal or state government health program. However, plans purchased through the ACA marketplace (Health Exchange plans), Federal Employee Health Benefits (FEHB) plans, and state employee plans are explicitly not considered government programs for the purpose of these savings offers — patients on those plans are eligible. Many patients assume otherwise and miss the savings.

For eligible patients, enrolling in the manufacturer savings program is the single most impactful step before filling a first prescription.

Telehealth Platforms — Faster Access, Sometimes Lower Cash Prices

For patients without insurance — or with insurance that does not cover weight management GLP-1s — telehealth platforms offer a direct route to prescription, and in some cases, more predictable pricing.

Platforms such as Ro, Found, and Hims & Hers operate on a model where the subscription fee covers both the clinical consultation and ongoing prescriber access. Medication pricing is separate and varies by platform and drug. Some platforms have negotiated lower cash prices for branded medications, or offer access to compounded versions.

The practical advantages: no prior authorization, no step therapy, and a streamlined online experience. The limitations: you are typically paying out of pocket, and the medication cost still represents a significant monthly outlay.

Before starting any GLP-1 medication, the candidacy framework matters — who is a strong candidate, who is a moderate candidate, and who should not be on these medications. For the full clinical picture, see GLP-1 Medications: The Complete Guide for Non-Diabetics.

For patients who have been denied by insurance and are not eligible for savings cards, telehealth platforms — combined with GoodRx pricing — represent the most accessible cash-pay route.

GoodRx and Smart Pharmacy Shopping

GoodRx is not a savings card — it is a negotiated pricing network. By running a prescription through GoodRx at a participating pharmacy, patients can access prices that are sometimes significantly lower than list price. For GLP-1 medications, the savings vary by drug, dose, and location.

Costco pharmacy consistently appears among the lower-cost retail options for medications including GLP-1s. Costco’s pharmacy is accessible to non-members for prescription purchases in most states. Checking current pricing directly at Costco’s pharmacy website or in-store is recommended, as prices fluctuate.

The same prescription can cost meaningfully different amounts at different pharmacies. Before filling, it is worth comparing prices across at least two or three pharmacies in your area — using GoodRx, each pharmacy’s own pricing tools, or a direct call.

One important note: GoodRx pricing and insurance coverage cannot be combined. You use one or the other for a given fill. If your insurance tier price is higher than the GoodRx price, GoodRx wins.

Compounding After the Shortage — What Is Still Legal

The compounding landscape for GLP-1 medications has changed substantially since 2024, and the current rules are more restrictive than many patients realize.

The shortage timeline. The FDA officially resolved the tirzepatide shortage on December 19, 2024. Semaglutide followed a different path: enforcement discretion for compounders ended in April–May 2025, after a federal court denied a legal challenge from compounding pharmacies. Neither semaglutide nor tirzepatide currently appears on FDA’s drug shortage list or the 503B bulks list.

What 503B outsourcing facilities can no longer do. Large-scale compounding operations — known as 503B outsourcing facilities — are prohibited from producing semaglutide or tirzepatide. With both drugs off the shortage list and absent from the 503B bulks list, mass compounding is no longer legally permissible.

What 503A pharmacies can still do — with important limits. Smaller, patient-specific compounding pharmacies operating under section 503A can still compound these medications, but the conditions are narrow. The FDA requires: a valid prescription for an individual patient; documentation from the prescriber establishing a significant clinical difference from the commercially available product; and that the pharmacy does not compound essentially a copy of a commercial drug regularly or in inordinate amounts — the FDA has indicated it may take action when a compounder fills more than four prescriptions of a compounded GLP-1 per calendar month.

One combination under explicit FDA scrutiny: Semaglutide compounded with vitamin B12 (cyanocobalamin). The FDA has stated it may consider this combination essentially a copy of the commercially available product when the active ingredient amounts are within 10% of existing branded strengths and the route of administration is the same.

If compounding remains your most viable access route, ask your prescriber whether they can document a clinical rationale, and ask them to refer you to a 503A pharmacy they work with directly. Any source offering compounded semaglutide or tirzepatide without a prescription is operating outside the law, regardless of how it is marketed.

Medicare and Medicaid — A Different Calculation

Medicare and Medicaid patients are explicitly excluded from manufacturer savings card programs. But options exist.

Medicare: GLP-1s for obesity treatment are not currently covered under standard Medicare Part D. There is a meaningful exception: semaglutide is now covered when prescribed for cardiovascular risk reduction in patients with established cardiovascular disease and a BMI of 27 or higher. If this applies to you, ask your prescriber whether the cardiovascular indication qualifies.

Medicaid: Coverage is highly variable by state. Some state Medicaid programs cover GLP-1 medications for obesity; many do not. Check your state Medicaid formulary or ask your prescriber to do so on your behalf.

Patient Assistance Programs (PAPs): Both Novo Nordisk and Eli Lilly maintain programs for uninsured or underinsured patients who do not qualify for savings cards. These programs provide medication at no cost or significantly reduced cost based on income. Eligibility criteria and application processes are available on the manufacturers’ websites.

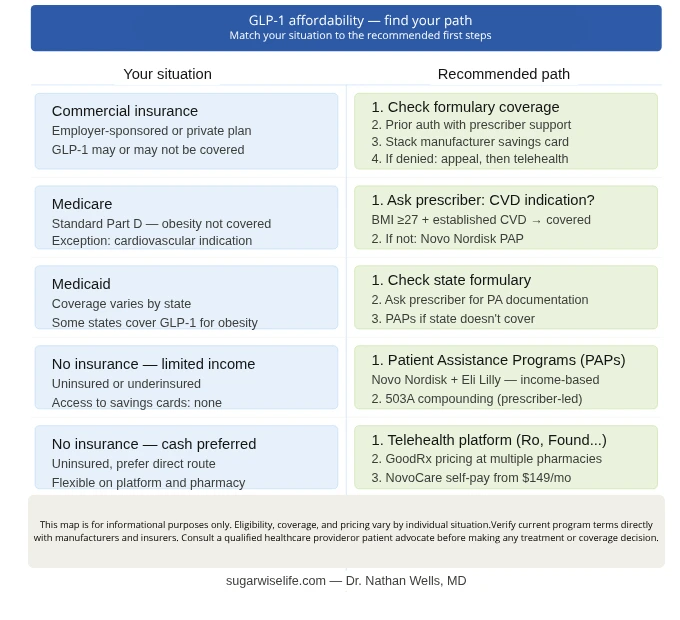

The Cheapest Way to Get GLP-1 — Based on Your Situation

There is no single cheapest option. There is the cheapest option for your situation.

You have commercial insurance: Check your formulary first. If covered, pursue prior authorization. Stack the manufacturer savings card on top. If denied, appeal — and consider a telehealth platform as a backup.

You have Medicare: Ask your prescriber whether you meet the cardiovascular indication for semaglutide coverage. If not, investigate the Patient Assistance Program.

You have Medicaid: Check your state formulary. Ask your prescriber for documentation support if prior authorization is required.

No insurance, income is limited: Patient Assistance Programs are the primary route. Compounding from a legitimate 503A pharmacy may also be an option with prescriber support.

No insurance, prefer a direct cash route: Telehealth platforms combined with GoodRx pricing represent the most streamlined path. Compare platforms, compare pharmacies, and factor in the consultation fee.

Frequently Asked Questions

How cheap can I get a GLP-1 without insurance?

Without insurance, your cost depends on the path you choose. Telehealth platforms offer cash pricing that varies by platform and drug. GoodRx can reduce pharmacy costs meaningfully. Patient Assistance Programs from Novo Nordisk and Eli Lilly provide medication at no cost for qualifying patients with limited income. Compounded semaglutide or tirzepatide through a legitimate 503A pharmacy — with a valid prescription — may offer the lowest cash price for those who qualify medically.

How much is GLP-1 at Costco?

Costco pharmacy typically offers competitive pricing on branded GLP-1 medications compared to other retail pharmacies, and is accessible to non-members in most states for prescription purchases. Prices fluctuate, so checking current pricing directly at Costco pharmacy or via their online tool is the most accurate approach. GoodRx pricing applied at Costco may reduce costs further.

What is the cheapest GLP-1 injectable?

Among branded options currently FDA-approved for weight management, Zepbound (tirzepatide) typically carries a lower list price than Wegovy (semaglutide 2.4 mg). However, with manufacturer savings cards, the out-of-pocket cost for either may be comparable for commercially insured patients. Compounded semaglutide or tirzepatide from a legitimate 503A pharmacy represents the lowest cash-pay option for patients who qualify medically.

How to make GLP-1 more affordable?

The four levers are: (1) insurance prior authorization with prescriber documentation support; (2) manufacturer savings card enrollment — commercial insurance only; (3) pharmacy shopping and GoodRx pricing; and (4) Patient Assistance Programs for uninsured or underinsured patients. Most patients who pay full price are missing at least one of these levers.

The Map Is Yours

The door metaphor holds all the way through. Most patients who stop GLP-1 therapy because of cost stopped at the first door — the sticker price — without knowing the others existed. Savings programs, telehealth access, smarter pharmacy choices, legitimate compounding, and patient assistance programs are not loopholes. They are part of the system, waiting to be used.

Price is a variable. The prescription is only the beginning of the calculation. What comes after depends on which doors you know to knock on — and now you have the map.

— Dr. Nathan Wells, MD

Physician | 25+ years in clinical and pharmaceutical medicine

Take good care.

References

2. Novo Nordisk. Wegovy Savings Card Program.

3. Eli Lilly. Zepbound Savings Card Program.

Want practical metabolic health insights, weekly? No noise — just evidence-based clarity from a physician. → Subscribe to the SugarWiseLife weekly briefing

Medical Disclaimer

This article is for informational purposes only and does not constitute medical advice. The content on SugarWiseLife.com is intended to support, not replace, the relationship between you and your healthcare provider. Dr. Nathan Wells is a pen name used for privacy purposes. Nothing in this article should be used to diagnose or treat a medical condition. Always consult a qualified healthcare professional before making changes to your diet, exercise routine, or medication.